#3 US Treasuries, War Bonds, Inverted Yield Curves, and Bank Runs

What do the terms mean? Why are Treasuries considered safe? Why did Great-Grandpa buy war bonds? What are the inverse relationships? What's an inverted yield curve ? What happened to SVB?

Listen to this post below

Q: What do these terms mean: US Treasury marketable securities/Treasuries and yield?

A: A US Treasury marketable security or “treasuries” is a broad term for when you or a bank loan the government money and it promises to pay you a yield, which is your return including the amount plus interest payments.12

Q: Why are Treasuries offered and why are they considered safe?

A: Treasury securities are generally considered very secure, as the name implies, because they are backed by the “Full Faith and Credit” of the government implied by the Constitution.34 The US government has never defaulted on its debt, and does not plan to (more on the often referenced debt ceiling another time).

Treasuries are also seen as safe because the United States Dollar (USD) is the world’s reserve currency, accounting for 59% of reserves held by all central banks (the Euro is second with 20%).5 Japan is the first largest foreign holder of US Treasuries followed by China, both with over $1T in American dollars.6 More for another time on the Dollar discussion.

Governments offer securities for a variety of reasons, including to reduce the amount of money in circulation in order to reduce inflation (contractionary monetary policy), as well as to fund spending that stimulates economic growth measured by gross domestic product (GDP).

Q: Why did Great-Grandpa buy war bonds?

A: Bonds play a big role in the psyche of Americans due to war dating back to the Revolutionary War. But the first case of Treasury bonds was in 1917 with the First Liberty Loan Act to fund the Great War (World War I).7

After the bombing of Pearl Harbor, America entered World War II, and the US issued and heavily advertised war/liberty/victory/defense/younameitwegotit! bonds to raise funds for military spending to win. For Americans, bonds became a way to show patriotism and feel the promise of stability in uncertain times.8

Since the 1950s, Treasuries have become more common place as just another tool for everyone to make money.9

Q: What do these other terms mean: coupon, maturity, T-bill, note, bond, and TIPS?10

A: Maturity refers to the length of time you hold the Treasury until you are paid the yield.

A Treasury bill or T-bill is purchased for the short term, meaning you can collect on the full amount anywhere from 4 weeks to 1 year. Interest is only paid at the end. T-bills are bought in $100 increments at a discount rate, meaning to earn 5% interest, you pay $95 first to receive $100 later.11

Treasury notes are purchased for the medium term from 2-10 years, and pay interest to banks or investors every 6 months. A frequently used term is coupon, which is a promise of regular interest rates paid out to the investor throughout the period.

Treasury bonds are purchased for 20 to 30 years, and pay interest every 6 months.

So if I buy a 20 year Treasury bond for $100 with a 5% yield, I am promised $105 in 2043, in addition to agreed upon interest payments every 6 months.12

Then there are TIPS (Treasury inflation protected securities), which protect against inflation for terms of 5, 10, and 30 years. These pay an interest rate every 6 months and also adjust your principal to what it is currently worth with inflation. TIPS sound amazing and like solutions to the other Treasuries, but come with drawbacks that you can read up on in the footnotes.1314

Q: What is the relationship between interest rates, bond prices, and yields?

A: There is an inverse relationship between interest rates and bond prices as well as bond prices and yields.15

The Federal Reserve directs the setting of interest rates. See my first post for more about interest rates!

As interest rates rise, existing bond prices fall, and vice versa. This is somewhat counter intuitive to normal supply and demand, where if more people want the same product, the price rises. If you already own a pair of shoes that become more popular, they become worth more.

But in dealing with promises on loans, you have to consider the government changing interest rates. As interest rates rise, the yields for new loans rise, while the yield you were already promised is worth less. The government promised you it would pay you back 5% on your $100, but now it is offering people 6% for $100. Your security is worth $1 less, and so if you re-sell it, it is worth less. The reverse is true as well.

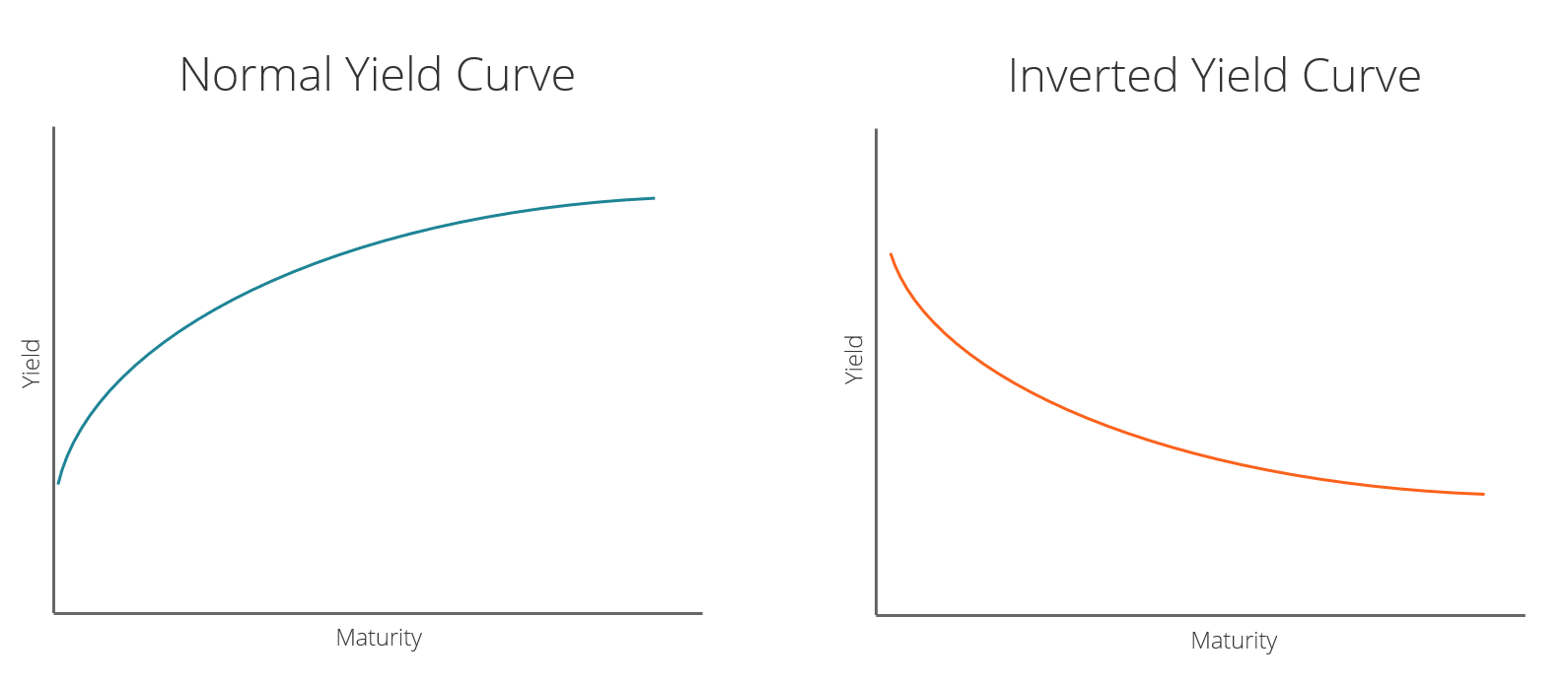

Q: What is the normal yield curve and what does it mean?

A: A normal yield curve graphs time on the horizontal end and interest on the vertical end. The takeaway is shorter term Treasuries promise lower yields and long term Treasuries promise higher yield.

The idea is that the present is relatively short and certain and the future is both longer and more uncertain. Where there is higher risk, there is higher return. In most periods of economic growth, this is the case.

Q: What is the inverted yield curve and what does it mean?

A: When the yield curve is inverted, short term Treasuries promise higher interest than long term Treasuries. In this scenario, the Fed has likely increased interest rates to decrease borrowing and reduce inflation, which can also encourage people to buy short term Treasuries. Or people may put their money in long term bonds because these are seen as safer than stocks. With extra demand, they accept lower yields.17 Or higher interest rates make short term Treasuries more attractive and investors do not want to take the risk with longer term repayments.

When the Federal Reserve hiked rates during the COVID-19 pandemic, the yield curve inverted. Short term Treasuries had higher yields than long term notes. Typically people refer to the 2 and 10 year Treasury notes.

Inverted curves are linked to recessions.18 Though currently inverted, there are signs that the curve is righting itself as the gap between yields narrows.19

Q: Putting it all together, what happened with Silicon Valley Bank (SVB) in terms of its Treasury holdings?

A: Hindsight is 20/22, but it is worth knowing what went wrong. WSJ does a great video that I’ll summarize along the lines of this post.20

Interest rates were near zero for the decade between 2008-2018. SVB became the favorite for entrepreneurs and venture capitalists in California because it offered really good service. Customers added about $189 bn in deposits. SVB needed a place to put this money where it would make some money, and so placed about $100 bn in what seemed like a very safe investment, long term Treasury bonds.

When interest rates rose rapidly in 2022, the yield curve inverted, and the price and therefore value of issued bonds fell. This led to unrealized losses of $17 bn. SVB sold bonds and realized $1.8 bn in losses to help shore up other aspects of its balance sheet. It stumbled with public messaging.21 But messaging aside, the financial oversight opened the bank to scrutiny for its leaders failing to act quickly enough to the rise in rates. Panicked start-ups and investors pulled their money out all at once.

JPMorgan Chase then absorbed SVB and another bank, First Republic.

For understanding a bank run in simpler times, and an homage to Axios Pro Rata’s posting, watch this scene from “It’s a Wonderful Life.”

Summary

What is old is new, because for the last twenty years, especially since the 2008 financial crisis, bonds have not really been on young people’s radar. Rates have been near zero, making borrowing cheap, and bonds unpopular. In addition, our investing horizon is long and the stock market has out-performed the bond market.22 With high interest rates, poor stock market performance, and low yield savings accounts, that calculus can change.

Understanding bonds can seem a little tricky, but when you think about the inverse relationships from the standpoint of already owning the bond, the government or bank offering someone else better terms helps it make sense.

Bank runs happen today and have happened throughout American history. A public bank’s board and leadership is elected by shareholders, and is in the fiduciary position to take care of its customers’ money. How creatively and quickly it responds to changes in government policy, as well as the way it communicates confidence, is very important.23

Behavioral economics can argue that people are rational or that they are irrational. A herd mentality where people follow the crowd fits both sides of that explanation. Sometimes the intelligent thing to do is to go with the herd, against the herd, or to act independently where one isn’t.

I hope you enjoyed! What are your thoughts?

https://www.treasurydirect.gov/marketable-securities/

https://www.sterling.com.jm/blog/difference-between-yield-and-interest-rate#:~:text=The%20key%20distinction%20between%20a,to%20measure%20your%20total%20return.

https://www.treasurydirect.gov/marketable-securities/

https://constitution.congress.gov/browse/article-4/section-1/#:~:text=Section%201%20Full%20Faith%20and,proved%2C%20and%20the%20Effect%20thereof.

https://crsreports.congress.gov/product/pdf/IF/IF11707

https://ticdata.treasury.gov/Publish/mfh.txt

https://www.investopedia.com/terms/l/liberty-bond.asp

War Bonds Explained Premier History, Youtube,

https://www.investopedia.com/ask/answers/033115/what-are-differences-between-treasury-bond-and-treasury-note-and-treasury-bill-tbill.asp

Jay Fairbrother, Everything You Need to Know about T-Bills, Youtube

https://www.fidelity.com/learning-center/smart-money/treasury-bills-vs-bonds#:~:text=Treasury%20bills%20have%20short%2Dterm,pay%20interest%20every%206%20months.

Jay Fairbrother, Are TIPS The Best Inflation Protection You Can Get? , Youtube,

https://www.investopedia.com/articles/investing/102215/3-reasons-stay-away-tips.asp

https://www.rba.gov.au/education/resources/explainers/bonds-and-the-yield-curve.html

https://corporatefinanceinstitute.com/resources/fixed-income/inverted-yield-curve/

https://www.forbes.com/sites/anthonytellez/2023/03/08/what-to-know-about-the-yield-curve-and-why-it-may-predict-a-recession/

https://www.forbes.com/sites/anthonytellez/2023/03/08/what-to-know-about-the-yield-curve-and-why-it-may-predict-a-recession/

https://www.wsj.com/livecoverage/stock-market-news-today-03-13-2023/card/yield-curve-inversion-unwinds-zEqHtaxQAoKpcXd1J6mF

How Silicon Valley Bank Collapsed in 36 Hours, Wall Street Journal, Youtube

https://www.goldmansachs.com/intelligence/pages/is-it-time-to-switch-from-stocks-to-bonds.html

Why should one care about bond prices if the purpose is to hold the bond to maturity?