#2 Interest Rates, The Fed, Inflation, Mortgages

What are the numbers? How is the Federal Reserve involved? What does this have to do with inflation and my mortgage?

Listen to this post below

Q: What are some current and historical interest rates for the US?

A: Current rate: 5%-5.25% (June 2023)

Rate one year ago in June 2022: 1.50-1.75%

Average since 1971: 5.42%1

Lowest rate: Close to zero in 2008 after the global financial crisis and in March 2020 at the outbreak of the COVID-19 pandemic

Highest rate: 19% for 1981 due to stagflation - combined high inflation, high unemployment, and low economic growth 23

Q: How is the Federal Reserve involved?

A: The Federal Reserve System (The Fed) is the U.S. Central Bank. The system oversees 12 banks spread across the country that provide financial services ranging from traditional savings accounts to home loans.

The Fed has what is called a dual mandate when it sets “monetary policy to promote maximum employment and stable prices”4

The Fed determines the federal funds rate 8 times per year, which affects the cost of borrowing for banks.

Specifically, the Fed changes the amount of interest banks earn from holding deposits with the Federal Reserve (Interest On Excess Reserves, IOER).

A higher interest rate means a commercial bank earns more money from holding their client’s deposits with the Federal Reserve versus making loans. For loans they do make, they change their rates to continue to make money.

On the other side, consumers have to save more as borrowing is expensive, and they find saving more attractive as banks offer better terms for deposits.5

Q: What is inflation?

A: Inflation is the economic condition where prices increase over time and the purchasing power of one dollar decreases.

Prices rise historically due to:

a) the rise in the costs of materials

b) the rise in demand as people have more income while chasing the same goods

c) the government increasing money in circulation, which makes each existing dollar worth less.6

Q: Why have inflation and interest rates been higher in the US recently?

A: The federal government added over 40% to the money supply quickly during the COVID-19 pandemic. Federal Reserve assets grew from $4.6T in March 2020 to $7.65T a year later. In the last 60 years, money supply increased on average around 7% a year.7 In part, this increase in money was because the Fed could not continue to lower near zero interests rates to make borrowing and spending more attractive.8

A further breakdown shows for around the initial increase, about $1.8T went to people and families, $1.7T went to businesses, and another $1T to government programs9

This made money more available and less valuable in a short period. As people with more money chased after the same goods like eggs and houses, the increased demand for those things led to an increase in prices, since there was not any increase in supply.

US inflation for 2022 averaged 6.5%, and over the last 12 months of rate hikes has averaged 4%. The annual target is 2% to avoid disproportionately high wages and prices that would cause businesses to hire less and consumers to spend less.

To deal with inflation, the US government signaled banks to raise interest rates by raising its federal funds rate, making it more expensive for consumers to borrow things like computers bought on credit cards or homes financed with mortgages. In general this causes a slow down of economic activity due to less spending and investment.

While two years ago, a standard loan for a house might have been 2%, today it is likely closer to 7%. That 5% of difference paid in interest to own a home over the course of 30 years is a significant amount.

Graphs

In economics, basic graphs explain most things, including interest rates and inflation well.

Below, an increase in the money supply (MS) lowers interest rates (i). In the US case, interest rates were already too low for more money in circulation to have much stimulus effect.10 Monetary policy that decreased the money supply then increased interest rates.

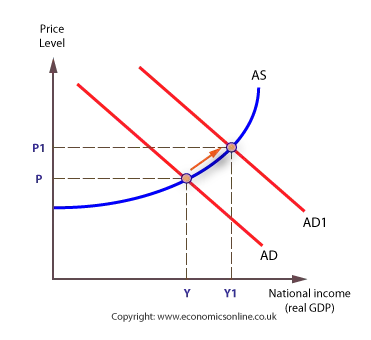

Below we see a shift right or increase in the aggregate demand (AD) in an economy, while the aggregate supply (AS) remains the same. Prices rise and gross domestic product (GDP) rises, and there is inflationary pressure.

Summary

Of course there is more to interest rates than what I outline in this post, but this is about the basics!

Understanding the range of borrowing costs your parents and grandparents experienced is important, because economic events often play out over and over, while people often have a short-term memory. Your grandparents likely took out a loan with a rate that was still significantly higher than today’s rates.

Understanding why the Fed changes rates is important to understanding how the government approaches inflation, and in turn what that means for your daily life.

I hope you enjoyed!

https://tradingeconomics.com/united-states/interest-rate

https://www.macrotrends.net/2015/fed-funds-rate-historical-chart

How Does Raising Interest Rates Control Inflation, The Economist, Youtube

https://www.federalreserve.gov/aboutthefed/files/the-fed-explained.pdf#page=Why Bond Yields Are An Important Economic Barometer, Wall Street Journal

How Does Raising Interest Rates Control Inflation, The Economist, Youtube

“What is Inflation” The School of Life, Youtube

https://usafacts.org/articles/what-is-the-money-supply-and-how-does-it-relate-to-inflation-and-the-federal-reserve/

https://www.investopedia.com/articles/economics/08/monetary-policy-recession.asp

https://www.nytimes.com/interactive/2022/03/11/us/how-covid-stimulus-money-was-spent.html

https://www.coursehero.com/sg/macroeconomics/the-equilibrium-interest-rate/